Working Capital Position

Richard Loth has 40+ years of experience in banking, corporate financial consulting, and nonprofit development assistance programs.

Updated June 30, 2021

Reviewed by

Reviewed by David Kindness

David Kindness is a Certified Public Accountant (CPA) and an expert in the fields of financial accounting, corporate and individual tax planning and preparation, and investing and retirement planning. David has helped thousands of clients improve their accounting and financial systems, create budgets, and minimize their taxes.

Trending Videos

For investors, the strength of a company’s balance sheet can be evaluated by examining three financial metrics: working capital adequacy, asset performance, and capitalization structure. In this article, we’ll start with a comprehensive look at how best to assess the company’s working capital position. In simple terms, this entails measuring the liquidity and managerial efficiency related to a company’s current position. The analytical tool employed to accomplish this task will be a company’s cash conversion cycle.

Don’t Be Misled By Faulty Analysis

To start this discussion, let’s first correct some commonly held, but erroneous, views on a company’s current position, which simply consists of the relationship between its current assets and its current liabilities. Working capital is the difference between these two broad categories of financial figures and is expressed as an absolute dollar amount.

Despite conventional wisdom, as a stand-alone number, a company’s current position has little or no relevance to an assessment of its liquidity. Nevertheless, this number is prominently reported in corporate financial communications such as the annual report and also by investment research services. Whatever its size, the amount of working capital sheds very little light on the quality of a company’s liquidity position.

Working With Working Capital

Another piece of conventional wisdom that needs correcting is the use of the current ratio and, its close relative, the acid test or quick ratio. Contrary to popular perception, these analytical tools don’t convey the evaluative information about a company’s liquidity that an investor needs to know. The often-used current ratio, as an indicator of liquidity, is seriously flawed because it’s conceptually based on the liquidation of all a company’s current assets to meet all of its current liabilities. In reality, this is not likely to occur. Investors have to look at a company as a going concern. It’s the time it takes to convert a company’s working capital assets into cash to pay its current obligations that is the key to its liquidity. In a word, the current ratio is misleading.

A simplistic, but accurate, comparison of two companies’ current positions will illustrate the weakness in relying on the current ratio and a working capital number as liquidity indicators:

| Liquidity Measures | Company ABC | Company XYZ |

| Current Assets | $600 | $300 |

| Current Liabilities | $300 | $300 |

| Working Capital | $300 | $0 |

| Current Ratio | 2:1 | 1:1 |

At first glance, company ABC looks like an easy winner in a liquidity contest. It has an ample margin of current assets over current liabilities, a seemingly good current ratio and a working capital of $300. Company XYZ has no current asset/liability margin of safety, a weak current ratio and no working capital.

However, what if both companies’ current liabilities have an average payment period of 30 days? Company ABC needs six months (180 days) to collect its account receivables, and its inventory turns over just once a year (365 days). Company XYZ’s customers pay in cash, and its inventory turns over 24 times a year (every 15 days). In this contrived example, company ABC is very illiquid and would not be able to operate under the conditions described. Its bills are coming due faster than it generates cash. You can’t pay bills with working capital; you pay bills with cash! Company XYZ’s seemingly tight current position is much more liquid because of its quicker cash conversion.

Measuring a Company’s Liquidity the Right Way

The cash conversion cycle (also referred to as CCC or the operating cycle) is the analytical tool of choice for determining the investment quality of two critical assets—inventory and accounts receivable. The CCC tells us the time (number of days) it takes to convert these two important assets into cash. A fast turnover rate of these assets is what creates real liquidity and is a positive indication of the quality and efficient management of inventory and receivables. By tracking the historical record (five to 10 years) of a company’s CCC and comparing it to competitor companies in the same industry (CCCs will vary according to the type of product and customer base), we are provided with an insightful indicator of a balance sheet’s investment quality.

Briefly stated, the cash conversion cycle is comprised of three standards: the so-called activity ratios relating to the turnover of inventory, trade receivables and trade payables. These components of the CCC can be expressed as a number of times per year or as a number of days. Using the latter indicator provides a more literal and coherent time measurement that is easily understood. The CCC formula looks like this:

DIO + DSO − DPO = CCC where: DIO = Days inventory outstanding DSO = Days sales outstanding DPO = Days payable outstanding \begin &\text-\text = \text\\ &\textbf\\ &\text\\ &\text\\ &\text\\ \end DIO + DSO − DPO = CCC where: DIO = Days inventory outstanding DSO = Days sales outstanding DPO = Days payable outstanding

Here’s how the components are calculated:

• Dividing average inventories by cost of sales per day (cost of sales/365) = days inventory outstanding (DIO).

• Dividing average accounts receivables by net sales per day (net sales/365) = days sales outstanding (DSO).

• Dividing average accounts payables by cost of sales per day (cost of sales/365) = days payables outstanding (DPO).

Liquidity Is King

One collateral observation is worth mentioning here. Investors should be alert to spotting liquidity enhancers in a company’s financial information. For example, for a company that has non-current investment securities, there is typically a secondary market for the relatively quick conversion of all or a high portion of these items to cash. Also, unused committed lines of credit—usually mentioned in a note to the financials on debt or in the management discussion and analysis section of a company’s annual report—can provide quick access to cash.

The Bottom Line

The old adage that «cash is king» is as important for investors evaluating a company’s investment qualities as it is for the managers running the business. A liquidity squeeze is worse than a profit squeeze. A key management function is to make sure that a company’s receivables and inventory positions are managed efficiently. This means making sure there’s an adequate level of product available and appropriate payment terms are in place, while at the same time making certain that working capital assets don’t tie up undue amounts of cash. This is an important balancing act for managers because, with high liquidity, a company can take advantage of price discounts on cash purchases, reduce short-term borrowings, benefit from a top commercial credit rating and take advantage of market opportunities.

The CCC and it’s component parts are useful indicators of a company’s true liquidity. In addition, the performance of DIO and DSO is a good indicator of management’s ability to handle the important inventory and receivable assets.

Cash Conversion Cycle: Definition, Formulas, and Example

Jim Mueller, CFA, began his career as a scientist. He has five years of experience as a senior analyst and another four years as a research analyst.

Updated June 28, 2022

Reviewed by

Reviewed by Amy Drury

Amy is an ACA and the CEO and founder of OnPoint Learning, a financial training company delivering training to financial professionals. She has nearly two decades of experience in the financial industry and as a financial instructor for industry professionals and individuals.

Fact checked by

Fact checked by Ryan Eichler

Ryan Eichler holds a B.S.B.A with a concentration in Finance from Boston University. He has held positions in, and has deep experience with, expense auditing, personal finance, real estate, as well as fact checking & editing.

Trending Videos

The cash conversion cycle is the amount of time a company needs or takes to convert funds invested in production and sales to cash. It is used to measure the company’s efficiency in using its working capital.

Learn more about the cash conversion cycle and how to calculate it and use it in an analysis.

Key Takeaways:

- The CCC indicates how fast a company can convert its initial capital investment into cash.

- Companies with a low CCC are often the companies with the best management.

- The CCC should be combined with other ratios, such as ROE and ROA, and compared with industry competitors for the same period for an adequate analysis of a company’s management.

What Is the Cash Conversion Cycle (CCC)?

The cash conversion cycle (CCC) is one of several metrics used to gauge how well management uses working capital. Working capital is the money used in day-to-day operations. This metric measures the amount of time a company takes to turn money invested in operations into cash.

The CCC uses the average times to pay suppliers, create inventory, sell products, and collect customer payments. Generally, the shorter this timeframe is, the better it is for the company.

Understanding the Cash Conversion Cycle (CCC)

The CCC combines several activity ratios involving outstanding inventory and sales, accounts receivable (AR), and accounts payable (AP). Outstanding inventory is inventory that has not been sold, accounts receivable are the accounts that the company needs to collect on, and accounts payable are accounts the company needs to make payments to.

To calculate CCC, you need to collect information from the company’s financial statements:

- Average inventory over the period

- Cost of goods sold or cost of sales

- Accounts receivable balance

- Annual revenue

- Ending accounts payable

You use this information to calculate days of inventory outstanding, days of sales outstanding, and days of payables outstanding.

Days of Inventory Outstanding (DIO)

DIO is how many days it takes to sell the entire inventory. The smaller the number, the better. To calculate it, you first need to determine average inventory:

(Beginning Inventory + Ending Inventory) / 2

Then, use it to calculate DIO:

Average Inventory / Cost of Goods Sold

Days of Sales Outstanding (DSO)

DSO is days sales outstanding or the number of days a company takes to collect on sales. First, calculate the average accounts receivable (AR):

Average accounts receivable ÷ 2

Then, calculate the DSO:

(Accounts Receivable / Annual Revenue) x Number of Days in Period

Days of Payables Outstanding (DPO)

DPO is days payable outstanding. This metric reflects the company’s payment of its own bills or accounts payable (AP). If this can be maximized, the company holds onto cash longer, maximizing its investment potential. Therefore, a longer DPO is better.

Ending Accounts Payable / (Cost of Sales / Number of Days)

Cash Conversion Cycle

You then use the value for each element to calculate the Cash Conversion Cycle:

Days inventory outstanding + Days sales outstanding — Days payables outstanding

Example of the Cash Conversion Cycle

Here’s an example—the data below are from the financial statements of a fictional retailer, Company X. All numbers are in millions of dollars.

| Item | Fiscal Year 2020 | Fiscal Year 2021 |

| Revenue | 9,000 | Not needed |

| COGS | 3,000 | Not needed |

| Inventory | 1,000 | 2,000 |

| AR | 100 | 90 |

| AP | 800 | 900 |

| Average Inventory | (1,000 + 2,000) / 2 = 1,500 |

| Average AR | (100 + 90) / 2 = 95 |

| Average AP | (800 + 900) / 2 = 850 |

Now, using the above formulas, the CCC is calculated:

- DIO = ($1,500 / $3,000) x 365 days = 182.5 days

- DSO = ($95 / $9,000) x 365 days = 3.9 days

- DPO = $850 / ($3,000 / 365 days) = 103.4 days

- CCC = 182.5 + 3.9 — 103.4 = 83 days

Using the Cash Conversion Cycle

On its own, CCC does not mean very much. Instead, it should be used to see if a company is improving over time and to compare it to its competitors. During an analysis, the CCC should be combined with other metrics—such as return on equity (ROE) and return on assets (ROA)—and can be useful when comparing competitors. The company with the lowest CCC is often—but not always—using its resources more efficiently.

Evaluating a Company

The CCC over several years can reveal an improving or worsening value when tracked over time. For instance, imagine Company X’s CCC was 83 days for the fiscal year 2020. In 2021, the company had a CCC of 130—this is a decline between the ends of fiscal years 2020 and 2021.

You might think that the change between these two years is significant—and it is, but it should indicate to you that you should investigate more to find out what might have happened. Examine external influences like market and economic conditions to see if something affected sales. You may need to look at the separate elements of the calculation to determine what happened—suppliers or customers could have financial problems that affected payments, raw material shortages, or transportation issues that affected deliveries.

You should also compare CCC changes over periods of several years to obtain the best sense of how a company is changing.

Evaluating Competitors

CCC should also be calculated for the same periods for the company’s competitors to establish a comparison. For example, imagine Company X’s CCC for the fiscal year 2021 was 130, and its direct competitor Company Y had a CCC of 100.9 days.

Compared with Company X, Company Y is doing a better job. It might be moving inventory quicker (a lower DIO), collects what it is owed faster (a lower DSO), or keeping its money longer (a higher DPO). However, remember that CCC should not be the only metric used to evaluate the company or the management; return on equity and return on assets are also valuable tools for determining management’s effectiveness.

To make things more interesting, assume that Company X has an online retailer competitor, Company Z. Company Z’s CCC for the same period is negative, coming in at -31.2 days. This means that Company Z does not pay its suppliers for the goods it buys until after it receives payment for selling those goods. Therefore, Company Z does not need to hold much inventory and still holds onto its money for a longer period. Online retailers usually have this advantage in terms of CCC, which is another reason why CCC should not be used in isolation without other metrics.

Special Considerations

The CCC is one of several tools that can help you evaluate performance, particularly if it is calculated for several consecutive periods and competitors. Decreasing or steady CCCs are a positive indicator, while rising CCCs require a little more digging.

CCC can also be applied to consulting businesses, software companies, insurance companies, or other companies without inventories. You’ll get a negative result similar to the online retailer because you omit days inventory outstanding.

What Is the Cash Conversion Cycle Formula?

The formula for the cash conversion cycle is:

Days inventory outstanding + Days sales outstanding — Days payables outstanding

What Does Cash Conversion Cycle Mean?

The cash conversion cycle measures the amount of time it takes a business to convert resources to cash.

What Is a Good Cash Conversion Cycle Number?

Cash conversion cycles depend on industry type, management, and many other factors. However, the fewer days it takes to convert resources to cash, the better it is for the business.

Цикл конвертации наличных денег (CCC): формула и как рассчитать цикл конверсии наличных денег

Вы когда-нибудь задумывались о том, как вырастет ваш бизнес, просто зная, когда продавать товарно-материальные запасы, собирать дебиторскую задолженность и когда ваша компания будет оплачивать счета без каких-либо штрафов? Теперь это то, что вы не хотите пропустить. Однако, чтобы вы знали вышеизложенное, вам нужно знать корень. а именно: цикл конвертации наличных, формула, отрицательный цикл конвертации наличных, расчет и как его рассчитать !. Это статья, которую вы не хотите пропустить, так что сидите смирно и получайте информацию.

#1.Что такое цикл конвертации наличных денег (CCC)?

Цикл конверсии денежных средств (CCC) — это показатель, который показывает, сколько времени требуется компании (измеряется в днях), чтобы преобразовать свои инвестиции в запасы и другие ресурсы в прибыль. денежные потоки от продаж. Кроме того, CCC, также известный как чистый операционный цикл, обычно направлен на оценку того, как долго каждый чистый вложенный доллар заблокирован в производстве. И процесс продажи до того, как он превратится в наличные деньги.

Во-первых, CCC является одним из количественных показателей, используемых для оценки деятельности и управления компании. Тенденция к снижению или стабильным значениям CCC в разные периоды является здоровым признаком. Тем не менее, их рост должен побудить к дополнительным исследованиям и анализу, основанным на других соображениях. Наконец, важно помнить, что CCC применяется только к определенным отраслям, которые полагаются на управление запасами и связанные с ним процессы.

Важный факт о цикле конвертации наличных денег (ccc)

Прежде всего, цикл конверсии денежных средств (CCC) — это показатель, который выражает время, необходимое компании (в днях). Превратить свои инвестиции в запасы и другие ресурсы в денежные потоки от продаж.

Во-вторых, эта метрика учитывает время, необходимое для продажи запасов, сбора дебиторской задолженности, а также количество времени, которое компания должна оплатить по своим обязательствам без штрафных санкций.

Наконец, исходя из характера корпоративной деятельности, CCC будет отличаться в зависимости от отрасли.

#2. Формула цикла конвертации наличных денег (CCC)

Ниже приведены формулы цикла конвертации наличных и значение каждой из них. Пойдем!

- Доступные запасы (DIO): среднее количество дней, которое требуется компании, чтобы преобразовать свои запасы в продажи. DIO — это среднее количество дней, в течение которых компания хранит свои запасы перед их продажей.

- Дни невыплаченных продаж (DSO): среднее количество дней, которое требуется предприятию для возмещения своей дебиторской задолженности. В результате DSO рассчитывает среднее количество дней, которое требуется компании для получения платежа после продажи.

- Дни погашения задолженности (DPO): это среднее количество дней, которое требуется корпорации для погашения своей кредиторской задолженности. В результате DPO рассчитывает среднее количество дней, которое требуется компании для оплаты счетов торговым кредиторам, т. е. поставщикам.

Мы можем поставить формула на три этапа, чтобы разбить его на части для лучшего понимания.

Первый этап формулы цикла преобразования наличности — это (DIO) дней хранения запасов, которые рассчитывают, сколько времени потребуется компании, чтобы продать свои запасы.

Второй этап — это (DSO) количество дней продаж, которые должны быть рассчитаны для расчета продолжительности времени, необходимого для получения денежных средств от этих продаж.

Последний этап — это (DPO) количество дней, подлежащих оплате, оно указывает, сколько времени требуется компании для оплаты своим поставщикам.

#3.Что означает отрицательный цикл конверсии денежных средств?

Отрицательный цикл конверсии денежных средств просто означает, что вам требуется больше времени для оплаты счетов/поставщиков, чем для продажи вашего продукта и получения ваших денег, подразумевая, что ваши поставщики финансируют ваш бизнес.

В этом случае корпорация фактически получает оплату за продаваемую продукцию до того, как она заплатит своим поставщикам за материалы. Более того, это может быть так, быстро продавая продукты, быстро собирая платежи с клиентов, а затем расплачиваясь с поставщиками компании. Следовательно, отрицательный цикл конверсии денежных средств обычно связан со сверхэффективными интернет-магазинами.

Следовательно, отрицательный цикл преобразования наличности может помешать вашей способности развивать и привлекать новых клиентов. Если ваш CCC положителен, как потребители, так и поставщики могут захотеть иметь с вами дело.

#4.Как рассчитать цикл конвертации денежных средств

Понимание всего, что связано с расчетом, обычно является первым шагом к тому, как рассчитать цикл конвертации наличных денег.

Чтобы предоставить информацию для расчета, вам необходимо обратиться к своим финансовым отчетам, таким как баланс и отчет о прибылях и убытках. Давайте посмотрим, как рассчитать три этапа цикла конвертации наличных денег.

Незавершенные запасы дней — это первый компонент уравнения (DIO). Это среднее время, за которое запасы превращаются в готовую продукцию и продаются.

DIO = (средний запас, деленный на стоимость проданных товаров), умноженный на 365.

Средний запас вашего периода (в стоимостном выражении) равен сумме ваших начальных инвентаризация стоимость и конечная стоимость инвентаря ÷ 2.

(Начальный инвентарь + Конечный инвентарь) ÷ 2

Себестоимость реализованной продукции составляет:

Покупки + начальный запас = конечный запас

Продажи в днях (DSO) — это среднее количество дней, в течение которых ваша дебиторская задолженность (деньги, причитающиеся вашему бизнесу) ожидает погашения.

DSO = (дебиторская задолженность, деленная на чистые продажи в кредит), умноженная на 365.

Дебиторская задолженность этого элемента представляет собой среднее значение начальной и конечной дебиторской задолженности.

(Начальная дебиторская задолженность + Конечная дебиторская задолженность) ÷ 2

Дни погашения задолженности (DPO) — это среднее время, которое требуется компании, чтобы закупить у своих поставщиков кредиторскую задолженность (ваша компания должна деньги) и оплатить их.

DPO — это аббревиатура от Ending Accounts кредиторской задолженности (себестоимость проданных товаров, разделенная на 365).

Кредиторская задолженность по этому элементу представлена следующим образом:

(начало к оплате + окончание к оплате) ÷ 2

Теперь вы можете рассчитать CCC после того, как закончите с Расчет цикла конвертации денежных средств на трех необходимых элементах формулы.

Расчет цикла конвертации денежных средств (CCC)

DIO + DSO минус DPO

#5.Как улучшить CCC

Компании могут сосредоточиться на любом из трех компонентов CCC, чтобы повысить (понизить) его. Однако увеличение DPO, уменьшение DSO или уменьшение DIO приведет к снижению CCC. Таким образом, компании могут улучшить CCC различными способами:

- Увеличьте скорость, с которой запасы конвертируются в продажи.

- Сбор оплаты от клиентов как можно скорее.

- Увеличьте время, необходимое для оплаты поставщикам.

Кроме того, жизненно важно признать, что CCC компании не существует независимо. Потому что он определяет, как компания взаимодействует со своими поставщиками и потребителями. В результате, если компания задерживает оплату своим поставщикам, эти поставщики будут страдать от негативного влияния на их цикл конвертации денежных средств из-за увеличения их DSO. В некоторых ситуациях у поставщиков могут возникнуть проблемы с денежными потоками, которые могут ограничить их способность выполнять заказы в срок.

В результате закупочные фирмы могут укрепить свои цепочки поставок, используя программы досрочной оплаты. Таким образом, поставщики могут получить досрочную оплату своих счетов от стороннего спонсора. В то время как компания оплачивает счет на более поздний срок. Как покупатель, так и поставщик могут извлечь выгоду из этого типа решения с точки зрения оптимизации своего оборотного капитала.

Как CCC влияет на денежный поток?

Индикатор оборотного капитала, называемый циклом конвертации денежных средств (CCC), обычно называемый денежным циклом, измеряет, сколько дней требуется бизнесу для преобразования денежных средств в товарно-материальные запасы, а затем обратно в денежные средства в процессе продаж.

Соответствует ли Ccc операционному циклу?

Время, необходимое предприятию для обналичивания своих запасов, измеряется циклом преобразования денежных средств, иногда называемым чистым операционным циклом или денежным циклом. Денежный цикл рассчитывает, сколько времени требуется бизнесу, чтобы превратить каждый доллар чистых ресурсов, использованный при производстве и продаже его товаров, в деньги, которые депонируются на его банковский счет.

Что делает твердый CCC?

Хороший CCC тот, который краток. Вы хотите, чтобы цикл конвертации денежных средств был как можно меньше, чтобы управлять эффективной и прибыльной фирмой. В идеале вы должны стремиться приблизить его к 1, поскольку в этот момент ваша компания будет иметь отличную ликвидность, а ее операционный капитал не будет заблокирован в течение длительных периодов времени.

Как CCC влияет на денежный поток?

Он измеряет, насколько быстро бизнес может превратить наличные деньги в дополнительные наличные деньги. CCC выполняет это, отображая преобразование денежных средств или капитальных вложений в запасы и кредиторскую задолженность (AP), в продажи и дебиторскую задолженность (AR) и, наконец, обратно в денежные средства.

Что означает аббревиатура оборотного капитала Ccc?

Продолжительность наличных денег в оборотном капитале определяется циклом конверсии денежных средств (CCC). Он измеряет продолжительность времени, которое требуется бизнесу, чтобы превратить отток денежных средств в приток денежных средств, и, следовательно, продолжительность времени, необходимого для финансирования текущих обязательств и поддержания операций.

Что означает отрицательный CCC?

Инвентарь продается до того, как вам придется заплатить за него, когда цикл конвертации отрицательных денежных средств. Или, другими словами, ваши поставщики платят за деятельность вашей компании. Для многих организаций отрицательный цикл конвертации денежных средств идеален.

Заключение

Цикл преобразования денежных средств (CCC) — это просто показатель, который эта компания использует, чтобы показать, сколько времени требуется для преобразования ее инвестиций в запасы и другие ресурсы в денежные потоки от продаж.

Часто задаваемые вопросы о цикле конвертации наличных

Что подразумевается под циклом конвертации денежных средств?

Цикл преобразования денежных средств (CCC) — это показатель оборотного капитала, который показывает, сколько дней требуется компании для преобразования денежных средств в товарно-материальные запасы, а затем обратно в денежные средства в процессе продаж.

Что такое плохой цикл конвертации наличных?

Отрицательный цикл конверсии денежных средств означает, что их поставщики финансируют их операции.

что такое хороший коэффициент конвертации наличных?

Более высокий CCR (обычно выше 1.0x) лучше, чем более низкий CCR, поскольку он указывает на то, что бизнес может конвертировать большую часть своих доходов в денежные средства.

Как сократить цикл конвертации наличных?

Компании могут сократить этот цикл, запрашивая авансовые платежи или депозиты и выставляя счета, как только поступает информация о продажах. Вы также можете предложить небольшую скидку за досрочную оплату, скажем, 2%, если счет оплачивается в течение 10, а не 30 дней.

Как рассчитать CCC в финансовом менеджменте?

- период запасов = 365 / оборачиваемость запасов.

- период дебиторской задолженности = 365 / оборачиваемость дебиторской задолженности.

- операционный цикл = период запасов + период дебиторской задолженности.

- операционный цикл = (365 / (себестоимость проданных товаров / средний запас)) + (365 / (продажа в кредит / средняя дебиторская задолженность))

Как сократить цикл конвертации наличных?

Компании могут сократить этот цикл, запрашивая авансовые платежи или депозиты и выставляя счета, как только поступает информация о продажах. Вы также можете предложить небольшую скидку за досрочную оплату, скажем, 2%, если счет оплачивается в течение 10, а не 30 дней.

В чем разница между операционным циклом и денежным циклом?

Хотя оба цикла служат схожим целям, операционный цикл дает представление об эффективности работы компании, а денежный цикл дает представление о том, насколько хорошо компания управляет своим денежным потоком. Кроме того, на практике часто бывает так, что один цикл влияет на другой.

Статьи по теме

- ДНИ ВЫДАЮЩИХСЯ ПРОДАЖ — все, что вам нужно знать

- Контент-маркетинг: Best Easy Guide (+ бесплатный курс)

- Финансирование счетов против факторинга: обзор, различия и сходства

- ЦИФРОВОЙ МАРКЕТИНГ: определение, виды и стратегии

- Кассовый учет: лучшие методы кассового учета в 2022 году (+ подробное руководство)

CCC: Cash Conversion Cycle Simplified. [+Practical Examples]

The cash conversion cycle (CCC) – often known as the cash cycle – is a working capital indicator that measures how long it takes for a company to convert cash into inventory and then back into cash through the sales process. The lower the CCC, the less time a company’s cash is locked up in accounts receivable and inventories.

Basically, the CCC is a crucial indicator for companies that buy and manage inventory. This is because it indicates both operational and financial efficiency. It should, however, not be seen in isolation, but rather in conjunction with other financial indicators such as return on equity. It’s also worth noting that CCC isn’t a major consideration for all businesses, as not every company will have physical inventory.

Understanding the Cash Conversion Cycle (CCC)

The CCC is made up of multiple activity ratios that include accounts receivable, payable, and inventory turnover. AP is a liability, while AR and inventory are short-term assets. The balance sheet contains all of these ratios. In reality, the ratios show how well management is generating cash from short-term assets and liabilities. An investor can use this information to assess the company’s overall health.

But then, you may ask, “What are the business implications of these ratios?”

Cash flows fast through a firm if it sells what customers desire to buy. The CCC slows down if management fails to realize potential sales. For example, if too much inventory accumulates, cash is locked up in things that cannot be sold, which is bad for business. To move inventory rapidly, management must lower prices, perhaps losing money on the sale of its items.

If AR isn’t well-managed, the organization may have trouble collecting payments from customers. And because AR is essentially a loan to the consumer, the company loses money when they don’t pay on time. The longer a corporation has to wait for payment, the less money is available for further investments. Slowing down AP payment to suppliers, on the other hand, benefits the company because of the extra time it allows to put the money to better use.

The Cash Conversion Cycle’s Elements

Calculating the CCC may be daunting at first, but once you grasp the elements involved, it becomes much easier.

To make the calculations, you’ll need to consult your financial statements, such as the balance sheet and income statement. Meanwhile, the three major elements of the cash conversion cycle include, Days Inventory Outstanding, Days Sales Outstanding, and Days Payable Outstanding.

Days Inventory Outstanding

Days Inventory Outstanding is the first part of the equation (DIO). This is the average time for inventory to be converted into final products and sold.

DIO = (Average Inventory ÷ Cost of Goods Sold) x 365

But then the average inventory (in value) for the period will be an addition of the beginning inventory value and ending inventory value; then dividing the sum by 2

(Beginning Inventory + Ending Inventory) ÷ 2

The cost of products sold is calculated as follows:

Ending Inventory = Beginning Inventory + Purchases.

Days Sales Outstanding

Days Sales Outstanding (DSO) is the average number of days it takes for you to retrieve your accounts receivable (money owing to you).

DSO = (Net Credit Sales + Accounts Receivable) x 365

The average of your beginning and ending receivables is your accounts receivable for this section.

(Beginning Receivables + Ending Receivables) ÷ 2

Days Payable Outstanding

Days Payable Outstanding (DPO) is the average time it takes a firm to purchase goods and services from its suppliers on accounts payable (your company owes money) and pay for them.

DPO = Ending Accounts Payable ÷ (Cost of Goods Sold ÷ 365)

In this section, the accounts payable are:

(Beginning Payable + Ending Payable) ÷ 2.

What Constitutes a Satisfactory Cash Conversion Cycle?

A short cash conversion period is ideal.

If your CCC is low or (better still) negative, your working capital is not locked up for long periods of time, and your company has more liquidity. Many online businesses have low or negative CCCs because they drop-ship instead of retaining inventory. They receive immediate payment when customers buy things, and do not have to pay for inventory until customers have already paid them.

On the other hand, you don’t want your CCC to be too high if it’s a positive number. A positive CCC indicates how many days your company’s working capital is stranded as it waits for accounts receivable to be paid. If you sell things on credit and your customers need 30, 60, or even 90 days to pay you, you may have a high CCC.

Read Also: SHORT TERM DEBT: Definition, Examples, and Debt financing

However, you can shorten your company’s cash conversion cycle in a number of ways.

This is by making your accounts receivable procedure as efficient as possible, for starters. Remove any needless jargon from your bills and be explicit about what you’re billing for and the terms you’re requesting.

For the most part, you’ll receive payments faster if the buyer understands the invoice quickly. You can also reduce the CCC by requesting advance payments or offering a discount for paying early. Finally, staying on top of late payments by following up as soon as a payment is due is a good idea.

What Role Does Cash Flow Play?

The cash conversion cycle is a cash flow formula that determines how long it takes for your company to convert inventories and other assets into cash. To put it another way, the cash-to-cash cycle time is the interval between when you pay for inventory and when customers pay to replenish your company’s cash flow. Keeping cash flow positive in industries with high inventory and material demands, such as construction, can be the difference between taking on new clients and turning them away.

The conversion cycle calculation determines how long a company’s cash is held until it is recovered from clients and customers. Keeping a careful eye on the company’s CCC might help you keep track of its total finances as money comes in and goes out. If you’re confused about the differences between cash flow and profit, keep in mind that they’re not the same thing. While profit is the amount of money left over after a company’s expenses are paid at a fixed point in time, cash flow is flexible. It shows how much money is coming in and going out of a company.

What’s the Difference Between a Cash Conversion Cycle and an Operating Cycle?

Obviously, there’s a big difference between a cash conversion cycle and an operating cycle.

Simply put, an operating cycle is the number of days between when you buy goods and when clients pay for them. The cash conversion cycle is the number of days it takes for you to pay for inventory and receive payment from your clients.

Why is the Cash Conversion Cycle so important?

There are various reasons why keeping track of your cash conversion cycle is critical.

For starters, investors, lenders, and other sources of capital frequently examine a company’s cash conversion cycle to gauge its financial health and, in particular, its liquidity. A company’s liquidity determines how readily it can repay a corporate loan, satisfy other financial obligations, and invest in growth. Furthermore, the cash conversion cycle is particularly useful for evaluating inventory-based enterprises like shops. However, it is not the only financial criterion used by lenders; they often mix it with other factors before determining whether or not to give out the loan.

Suppliers may consider your CCC while considering whether or not to grant credit to your business. They are often concerned that you may not be able to pay them on time if your company lacks appropriate liquidity.

Read Also: Debt To Equity Ratio: Explained. Formula, Calculations, Examples

On the other hand, you should be concerned about the cash conversion cycle as well.

Like we earlier mentioned; a low CCC suggests that you’re doing a good job of converting inventory to cash and that your firm is running well. If your CCC is too high, however, it could indicate operational concerns, a lack of demand for your goods, or a shrinking market niche. So if your CCC isn’t to your liking, determine what’s wrong and take steps to fix it, such as increasing your invoice collection efforts.

Finally, when determining how much money you need to borrow, your cash conversion cycle is a crucial factor to consider. Understanding your CCC and, as a result, your company’s liquidity, can assist you in determining how much cash you can request from a lender.

The Formula for CCC

Since CCC includes calculating the net aggregate time involved over the three stages of the cash conversion lifecycle mentioned above, the mathematical formula for CCC is:

CCC=DIO+DSO−DPO

where: DIO=Days of inventory outstanding(also known as days sales of inventory)

DSO=Days sales outstanding

DPO=Days payables outstanding

DIO and DSO represent cash inflows, whereas DPO represents cash outflows.

As a result, DPO is the sole negative number in the equation. Another way to look at the formula is that DIO and DSO are tied to inventory and accounts receivable, which are both considered short-term assets and are assumed to be positive. DPO is associated with accounts payable, which is a liability and consequently a negative number.

CCC Calculation

The cash conversion cycle of a business is divided into three parts. Several items from the financial accounts are required to compute CCC:

- The income statement showing revenue and cost of goods sold (COGS).

- The record of inventory at the start and end of the time period.

- Accounts receivable (AR) at the start and end of the time period

- Accounts payable at the start and end of the time period

- The number of days in the period (for example, a year is 365 days and a quarter is 90 days).

First Stage

The first stage is deals with the current inventory level and shows the time it will take for the company to sell its stock.

This value is comes from the Days Inventory Outstanding figure (DIO). Meanwhile, a lower DIO number is desirable because it implies that the company is making sales quickly, signifying a higher business turnover.

The cost of goods sold (COGS), which indicates the cost of obtaining or manufacturing the products that a company sells during a period, is is vital to calculating the DIO or DSI.

DSI= Avg. Inventory/ COGS ×365 Days

where: Avg. Inventory=21×(BI+EI)

BI=Beginning inventory

EI=Ending inventory

Second Stage

The second stage focuses on current sales and shows how long it takes to collect the sales proceeds.

Days Sales Outstanding (DSO) is a metric that divides average accounts receivable by revenue each day to arrive at this value. DSO with a lower value shows that the company is able to collect funds in a timely manner, so improving its cash position.

DSO= Revenue Per Day / Avg. Accounts Receivable

where: Avg. Accounts Receivable=21×(BAR+EAR)

BAR=Beginning AR

EAR=Ending AR

Third Stage

The third step focuses on the company’s current overdue payables. It indicates the amount of money a company owes its current suppliers for inventory and items purchased, as well as the time frame in which those commitments must be met.

Days Payables Outstanding (DPO), which considers accounts payable, is helps to determine this number. It is preferable to have a greater DPO value. By increasing this amount, the corporation may keep its capital for longer, allowing it to invest more.

DPO= COGS Per Day / Avg. Accounts Payable

where: Avg. Accounts Payable=21×(BAP+EAP)

BAP=Beginning AP

EAP=Ending AP

COGS=Cost of Goods Sold

All of the data above are accessible in a publicly-traded company’s financial statements. They are filed as part of its annual and quarterly reporting. For a year, the number of days in the corresponding period is 365, and for a quarter, it is 90.

What You Can Learn From the Cash Conversion Cycle?

The primary strategy for a company to increase profits is to increase inventory sales. But how can one increase sales? If cash is readily available at regular intervals, one can churn out more sales for profit, as more products to create and sell result from the frequent availability of money. Inventory can be purchased on credit, resulting in accounts payable (AP).

A business can also sell things on credit, resulting in receivables (AR). As a result, cash isn’t a consideration until the company pays its bills and collects its receivables. This means that cash management relies heavily on timing.

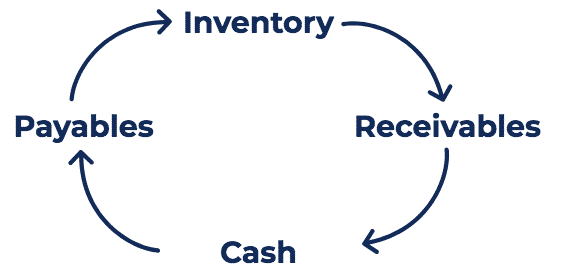

In other words, the lifespan of cash utilized for corporate activities is tracked by CCC. It tracks cash as it moves from cash in hand to inventory and accounts payable, then to product or service development expenses, sales and accounts receivable, and finally back to cash in hand.

Read Also: CHECK FORMAT: EXAMPLES, PROPER FORMAT, ROUTING NUMBERS & ALL YOU NEED

CCC is a measure of how quickly a corporation can convert invested cash from start (investment) to finish (exit) (returns). Again, the CCC should be as low as possible.

The three key ingredients of business are inventory management, sales realization, and payables. The business will suffer if any of these go out the window—for example, inventory mismanagement, sales restrictions, or payables increasing in number, value, or frequency. CCC accounts for the time spent in various procedures in addition to the monetary value, providing a different perspective on the company’s operational efficiency.

In general, the CCC value, in addition to other financial measurements, reveals how well a company’s management is using short-term assets and liabilities to generate and redeploy cash. It provides insight into the company’s financial health in terms of cash management. The graph also aids in determining the liquidity risk associated with a company’s operations.

Example

Let’s work through this using a hypothetical example. The information below comes from the financial accounts of Company X, a fictional retailer. All figures are expressed in millions of dollars.

| Item | Fiscal Year 2021 | Fiscal Year 2022 |

| Revenue | 9,000 | Not needed |

| COGS | 3,000 | Not needed |

| Inventory | 1,000 | 2,000 |

| A/R | 100 | 90 |

| A/P | 800 | 900 |

| Average Inventory | (1,000 + 2,000) / 2 = 1,500 |

| Average AR | (100 + 90) / 2 = 95 |

| Average AP | (800 + 900) / 2 = 850 |

The CCC is now calculated using the formulas above:

DIO = US$1,500 / ($3,000/ 365 days) = 182.5 days

DSO = US$95 / ($9,000 / 365 days) = 3.9 days

DPO = US$850 / ($3,000/ 365 days) = 103.4 days

Therefore, CCC = 182.5 + 3.9 – 103.4 = 83 days

So, What’s Next?

As you know by now, CCC isn’t really significant on its own. It should instead be used to track a company’s performance over time and to compare it to its competitors.

When measured over multiple years, the CCC can reflect an improving or deteriorating value.

For example, if Company X’s CCC was 90 days in fiscal year 2023, the company has improved between the end of fiscal year 2023 and the end of fiscal year 2024

While the difference between these two years is positive, a considerable change in DIO, DSO, or DPO may warrant more study, such as a look back in time. So To get the best picture of how things are changing, look at CCC changes over multiple years.

For the same time periods, CCC should be determined for the company’s competitors.

For example, Company X’s competitor, Company Y’s CCC for fiscal year 2023 was 100.9 days (190 + 5 – 94.1).

Read Also: Accounts Payable vs Accounts Receivable Detailed Comparison

Company X outperforms Company Y in terms of moving goods (lower DIO), collecting what it owes (lower DSO), and keeping its own money for longer (higher DPO). However, keep in mind that CCC should not be the only statistic used to assess the company or management; ROE and ROA are also useful tools for measuring management effectiveness.

Assume that Company X has an online retailing competition, Company Z. This will make things more interesting. Company Z’s CCC over the same time period is -31.2 days, which is negative.

This means that Company Z does not pay its suppliers for the commodities it purchases until it is paid for the goods it sells. As a result, Company Z doesn’t need to keep as much inventory and can keep its money for longer. In terms of CCC, online retailers typically have an edge, which is another reason why CCC should never be utilized in isolation from other metrics.

Cash Conversion Cycle Specific Considerations (CCC)

The CCC is one of various tools that can be used to assess management, especially if it is measured over multiple eras and competitors. CCCs that are decreasing or constant are a good sign, whereas rising CCCs demand a little more investigation.

CCC is most effective when used by retail businesses with inventories that are sold to customers. Meanwhile, consulting firms, software firms, and insurance firms are all examples of enterprises for which this statistic is useless.

Negative Cash Conversion Cycle (CCC)

At the end of the day, a positive cash conversion cycle, even if low in comparison to comparable organizations, is still a “use” of capital. Certain companies might have negative CCCs, which indicates the net impact is a cash “source.” This is a rare occurrence. Turning over inventory frequently and getting cash payments for products sold before paying suppliers would result in a negative CCC.

Amazon is one of the most frequently mentioned examples of a company with a negative CCC. Due to the time lag, Amazon was able to effectively finance its operations by having a negative CCC, which allowed it to take advantage of attractive delayed payment terms with suppliers; but, unlike typical debt financing, this came with no interest.

This freely accessible capital helped support Amazon’s growth plans and had a significant part in developing the company into what it is today, despite the fact that it was an unsuccessful corporation with steep losses. Amazon had a substantially lower CCC that went below zero, even when compared to other market leaders such as Walmart, which are known for their efficiency.

What Is CCC?

The cash conversion cycle (CCC) – often known as the cash cycle – is a working capital indicator that measures how long it takes for a company to convert cash into inventory and then back into cash through the sales process.

What Are Examples of Negative CCC

Amazon is one of the most frequently mentioned examples of a company with a negative CCC. Due to the time lag, Amazon was able to effectively finance its operations by having a negative CCC, which allowed it to take advantage of attractive delayed payment terms with suppliers; but, unlike typical debt financing, this came with no interest.

How Does Cash Conversion Cycle Affect Profitability?

A low or (better still) negative CCC depicts a good conversion cycle. In this case, your working capital is not locked up for long periods of time, and your company has more liquidity. Many online businesses have low or negative CCCs because they drop-ship instead of retaining inventory.

What Are the 3 Components of the Cash Conversion Cycle?

There are 3 components to the cash conversion cycle:

- Days Inventory Outstanding (DIO).

- Days Sales Outstanding (DSO)

- .Days Payable Outstanding (DPO).

How Does CCC Affect Profitability?

As a measure of how liquid a company is, the cash conversion cycle (CCC) is the number of days that capital is tied up in business processes. Having a short cash conversion cycle instead of a lengthy one is seen as good for the profitability of a business.

Related Articles

- DAYS OF SALES OUTSTANDING- Everything You Need To Know

- Content marketing: Best Easy Guide (+ free course)

- Accounts Receivable: Examples, Process, Formula & Free Tips

- OUTSTANDING CHECKS: Overview(+How to Avoid Outstanding Checks)

Emmanuel Okpaku

As a seasoned business consultant, Emmanuel leverages over 6 years of experience helping startups and large organizations bring their visions to life across critical areas like business strategy, sales, marketing, branding, HR, and more. Emmanuel first cultivated this diverse skillset by launching and scaling his small business consultancy. As the sole founder, he handled all aspects of operations from attracting clients to project delivery and finance management. This first-hand experience as an entrepreneur informs the holistic guidance he now provides. Through individual business consulting and entrepreneurship education, he equips new founders with an adept understanding across essential domains – strategic planning, marketing, sales, HR, branding and beyond. He instills time-tested frameworks to set a strong foundation while retaining agility to pivot as needed. Whether helping ideate a startup from scratch or strengthening an existing small business, he provides road-tested wisdom so founders can bring their ambitious visions to fruition.